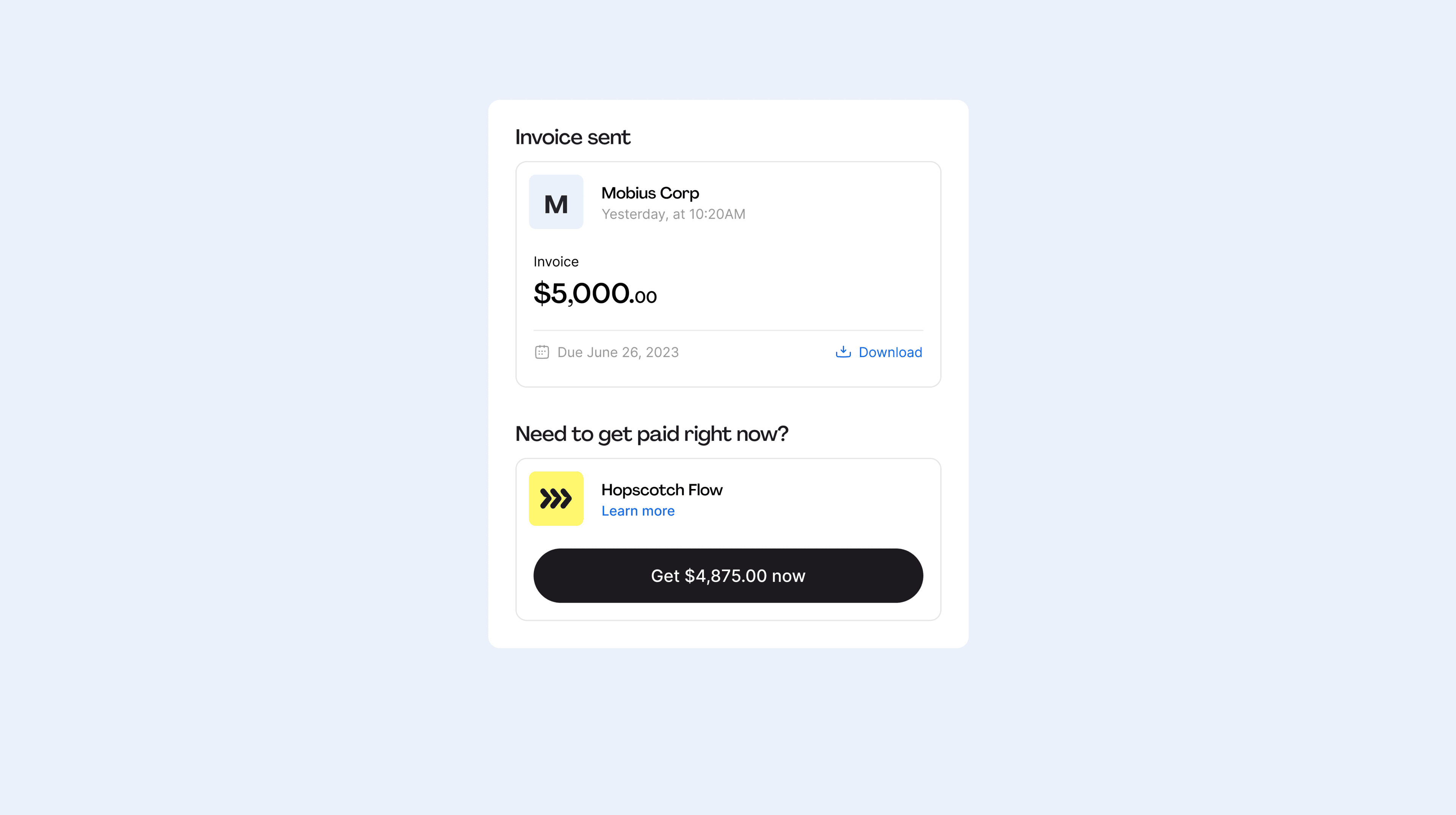

Businesses that use Hopscotch Flow get paid 41 days faster!Learn more

Products

Customers

Learn

Guides

December 17, 2021

Blog

6 minutes

10 minutes

5 min